The Third Opportunity to Get Rich Off Tesla

The first principles of AGI robots. Photos of solar roofing and my stock account

In an N-of-1 situation, reasoning by analogy doesn’t work. This essay looks under the hood of Tesla as an investment, using first principles and a dive into Elon’s AGI robot program, Optimus. I also revisit my experience working for Tesla, photos included. For dessert, we have screenshots of my brokerage account from 2019.

From ten years of playing with stocks, I have learned that very few people are interested in analyzing and modeling the business behind the stock. The stock market is not efficient. If I ACTUALLY TRY, it is possible to make above-average financial gains from investing in well-chosen equities. This is the path of most resistance.

As a teenager, I learned that the way to get rich is to own a business. The quickest way to own a business is to buy someone else’s. The quickest way to do that is public equities. This is not a game that I recommend unless you are wired for it. Years ago, I read a tweet thread called “How to Get Rich (without getting lucky)” by entrepreneur/investor Naval Ravikant. I agree with Naval when he says that to win big, you need to leverage specific knowledge. In this case, the leverage is capital and the specific knowledge is AI robotics.

Tesla is N of 1. Elon is N of 1. The only way to understand what’s going on is by reasoning from first principles, which is boiling things down to fundamental truths then reasoning from there. The Optimus section of this essay is an example of reasoning from first principles. Reasoning by analogy is ineffective in an N-of-1 situation. The market sucks at pricing an N-of-1 situation. Even institutional Ivy League money managers fall into the trap of reasoning by analogy. For years I heard, "Tesla is a car company and the other car companies make more cars and have lower valuations, therefore Tesla is overvalued." Reasoning from first principles is more difficult. It’s scary and requires creativity, courage, and conviction, similar to the kind that is required to build an N-of-1 company.

Right now, we are in between the third and fourth Tesla product generations. The market is relaxed between the ramp of Model 3/Y and the realization of the compact car/robotaxi platform and Optimus. The ramping of products, earnings, and stock price looks like a series of S-curves.

The realization of the original Tesla Roadster made Tesla worth $1-10 billion. The scaling of Model S and X made Tesla worth $10-100 billion. The Model 3 and Y made Tesla worth $100 billion to 1 trillion. The compact car and robotaxi will make Tesla worth $1-10 trillion. In the long term, hold on to your hat, Project Optimus and its descendants will make Tesla worth $10-100 trillion.

I don’t know when Tesla will achieve volume production and profitability of the fourth phase. I don’t know when the market will price those future earnings into the valuation. What I do know is that if some or all of the products come to fruition, I’d rather be invested multiple years early than one day late. It's worth repeating that for emphasis. When dealing with an asset that can rise 5-10x in a short period, I would rather be five years early than one day late.

Expected Value = Potential Value x Probability

What is the potential value of what Tesla is building and what is the probability that it comes to fruition for Tesla?

“The team was successful in the past therefore they will be successful in the future,” is an example of reasoning by analogy. Past performance does not guarantee future performance. Just look at the New England Patriots.

It’s tempting to think that because the Tesla team was successful in the past, they will be successful in the future. But other companies are poaching talent from Tesla and there’s more competition in the EV business. Also, Elon is getting increasingly political and he is working on many other projects. I can address each of these points in detail upon request in the comments. For now, I will jump to what matters most: Where do the smartest engineers want to work and who is on the team? Tesla and SpaceX are the top two most desired places to work for college engineering students.

Elon doesn’t give a shit about boundaries. His legion of elite engineers can and will work across the Musk empire: SpaceX, Tesla, X, X.AI, Neuralink, and Boring Company. Tesla uses materials originally developed at SpaceX. X utilized Tesla software engineers. Tesla can use data, software, and engineering talent from X and X.AI, for its Optimus humanoid worker bot and other AGI products.

The value of the Elon-empire’s AGI work will be most reflected in Tesla, as opposed to X, X.AI, SpaceX, or Neuralink, because Tesla is developing the best AI hardware — both the robotics for the frontend and the supercomputers for the backend AI training.

This post on X mostly flew under the radar. It’s a comment on a post about the Grok LLM created by X.AI. Elon is saying that if Tesla owns and operates a fleet of robot-taxis, those vehicles will only be driving for around 8 hours per day. Each vehicle will have a powerful AI computer that can be used for other purposes while the cars are idle. SETI — Elon’s example from the tweet — is a project that uses distributed computing to process space signals to look for aliens.

An analogy to the internet helps communicate what's developing in AI. For the internet, Apple built the best user-facing interfaces, and Amazon built the best backend with AWS and order fulfillment. Humanoid robots like Optimus, and AI-equipped cars like my Model Y, are physical extensions of AI, like an iPhone is the physical extension of the internet. Tesla’s Dojo supercomputer could power much of AI training like Amazon AWS powers much of the internet.

Optimus Humanoid Robot

What makes humans super-powerful creatures?

Thumbs

Vision

Walking

Talking

Memory

Thinking

Long-lasting battery, 8-hour recharge

That’s the recipe for an effective human worker. A factory that can spawn useful humanoid workers would be the most valuable product ever created and it’s not even close.

The global economy = Number of human workers X Output per worker

The number of human workers has been going up exponentially for 200 years, but that’s no longer the case. Elon and I have both written about the birth rate situation. Robots and software have been increasing the output per worker. But now we’re talking about a world where the robots and software ARE the workers.

The timing is beautiful. Earth’s human population is breaching an exponential decline, at the same time that the robot population is launching exponentially. That’s good for the financial numbers.

The new equation for the global economy = (Number of bots X Output per bot) + (Number of humans x Output per human)

This is a quasi-infinite situation. If robots can independently produce more robots then it’s unclear what the constraint is. The constraint could be something like desire, motivation, or inspiration to build more.

Development of human features in Optimus:

Hands: already unbelievably good

Walking: Yes, already doing yoga!

Talking: Speakers, microphones, and LLMs are already useful

Vision: Cameras are better than human eyeballs. Tesla FSD Beta is camera-only and can drive on city streets, albeit not 100% reliable. But it is safer than a human driver.

Memory: Computers have super-human memory

Thinking, planning, and execution: Tesla FSD Beta is probably the best example of real-world AI in operation. It’s tough to say when a neural net is “thinking” or not. What I think is that new capabilities will continue to emerge as computing power grows and data sets improve. The timing of when particular abilities emerge is unpredictable.

Battery and recharge: Is the energy density and recharge time adequate for a humanoid robot to do useful work shifts? If there’s a 250 kW supercharger around, then certainly yes. For a medium-large factory, it would make sense to install a supercharger. For a small business or a home using only a few Optimus bots then a 240 Volt outlet, a washer/dryer outlet, will need to be sufficient.

Right now I have Tesla’s “Full Self-Driving Beta” software on my car. The same tech is being used for Optimus. A big challenge with developing the robotaxi software is that humans are inside the robots. The bot can’t take risks and learn from in-real-life mistakes. “Move fast and break things” is not an option. The robotaxi needs to not only not crash, but also have a driving style that the human inside wants to be comfortable with. What’s more, outdoor conditions and roadwork situations are highly variable. A robot-taxi ride-hailing service is one application of AI robotics that is exceptionally difficult to realize; however, it’s worth the slog because the value to the market is tremendous.

On the other hand, humanoid robots working inside a factory can take more risks and work in a more controlled indoor setting. They can move fast and break things with less consequence, liability, and regulations, compared to robotaxis on public roads with customers inside.

The future is robots building more of themselves. A product that can build more of itself has never been built. This is an N-of-1 situation. It’s hard to imagine and then suddenly it’s not. We’ve replicated nearly all features of biological life.

Photosynthesis is solar

Muscles and joints are actuators

Mitochondria are battery cells

Eyes are cameras

Neural networks are neural networks

Ears are microphones

Voice boxes are speakers

Memory is memory

Veins and nerves are wires

The serious investor is looking closely at the capabilities of Optimus and what it takes to be able to assist or take over various jobs in the economy. How long before robots are working as drivers, roofers, chefs, servers, mailmen, and miners? How about security guards, or dare I suggest it, childcare? The ten most common jobs in America are cashier, food preparation worker, stocking associate, laborer, janitor, construction worker, bookkeeper, server, medical assistant, and bartender. It’s worth considering how much of the responsibilities of these roles can be shifted to Optimus this year, next year, and in 2030.

Project Optimus and its descendants have the potential to spawn a $10-100 trillion corporation. That would be larger than the United States GDP. There would be even more material abundance, comfort, and ease. The big question remains: What do you really want? What do WE really want?

Working for Tesla

Not everything at Tesla works out, but a lot of it does. Tesla Energy is a good example. I worked for Tesla on the Solar Roof project. It was disastrous. Some months after I quit, the Tesla solar roof program in Oregon was shut down. The 2023 Tesla solar installation numbers are poor. But the other side of Tesla Energy is the battery storage business and that’s been very successful. The utility-scale Megapack has been particularly profitable. The energy storage business will continue to grow, but it will be dwarfed by its AI robotics cousins.

Tesla, SpaceX, Elon, X and X.AI move fast and break things. I was a part of it. For better or worse, they have the fastest pace of innovation. They start early and run the fastest; that’s the horse I like betting on.

Stock Stuff

I’m not buying more Tesla stock right now because I’m already all in. As of writing this in November 2023, my media business is not cash flow positive, so consider joining paid subscribers. I hold Tesla shares. What I’m holding is the rights to the profits of a legion of robots. It’s possible that in the future it’s billions of bots earning tens of thousands of dollars each, per year. The exact numbers are unclear. But what is clear is that we’re talking trillions. And I like trillions. Because a teeny tiny share of trillions means I can continue to invest in writing projects and still eat high-quality food.

In 2019, I predicted in a blog post that in 2024 Tesla’s market cap will be $500 billion. It’s November 8, 2023, and Tesla is valued at $700 billion. I maintain that at some point in 2024, the company will be valued at $500 billion. High interest rates on car loans increase the cost of buying a Tesla vehicle. Tesla dropped prices to maintain high sales growth, which eats into profitability. Simultaneously there is an economic slowdown. On top of that, EV subsidies are being reduced and there’s a pull forward of demand into Q4 2023. Meanwhile, Tesla is investing in new product development, like Optimus and Dojo, and factory development for the Cybertruck, compact car and robotaxi production. These are big expenses. All of these factors create a lull in profitability, fueling a “busted growth story” narrative. If history repeats itself then short-sellers, who previously got wrecked by Tesla, will be back again to pull the stock price down, then get wrecked again.

From my old blog, posted on May 31, 2019:

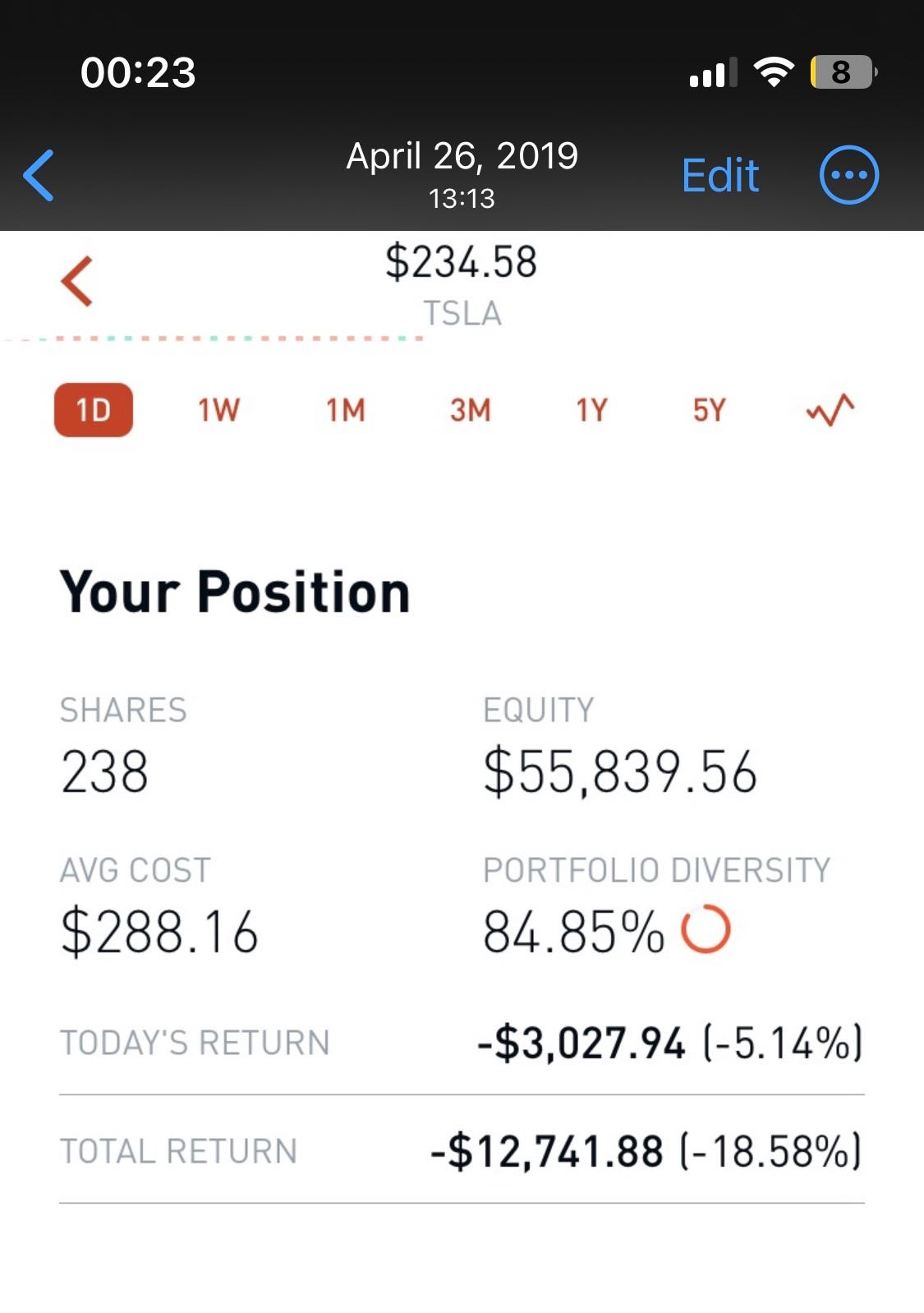

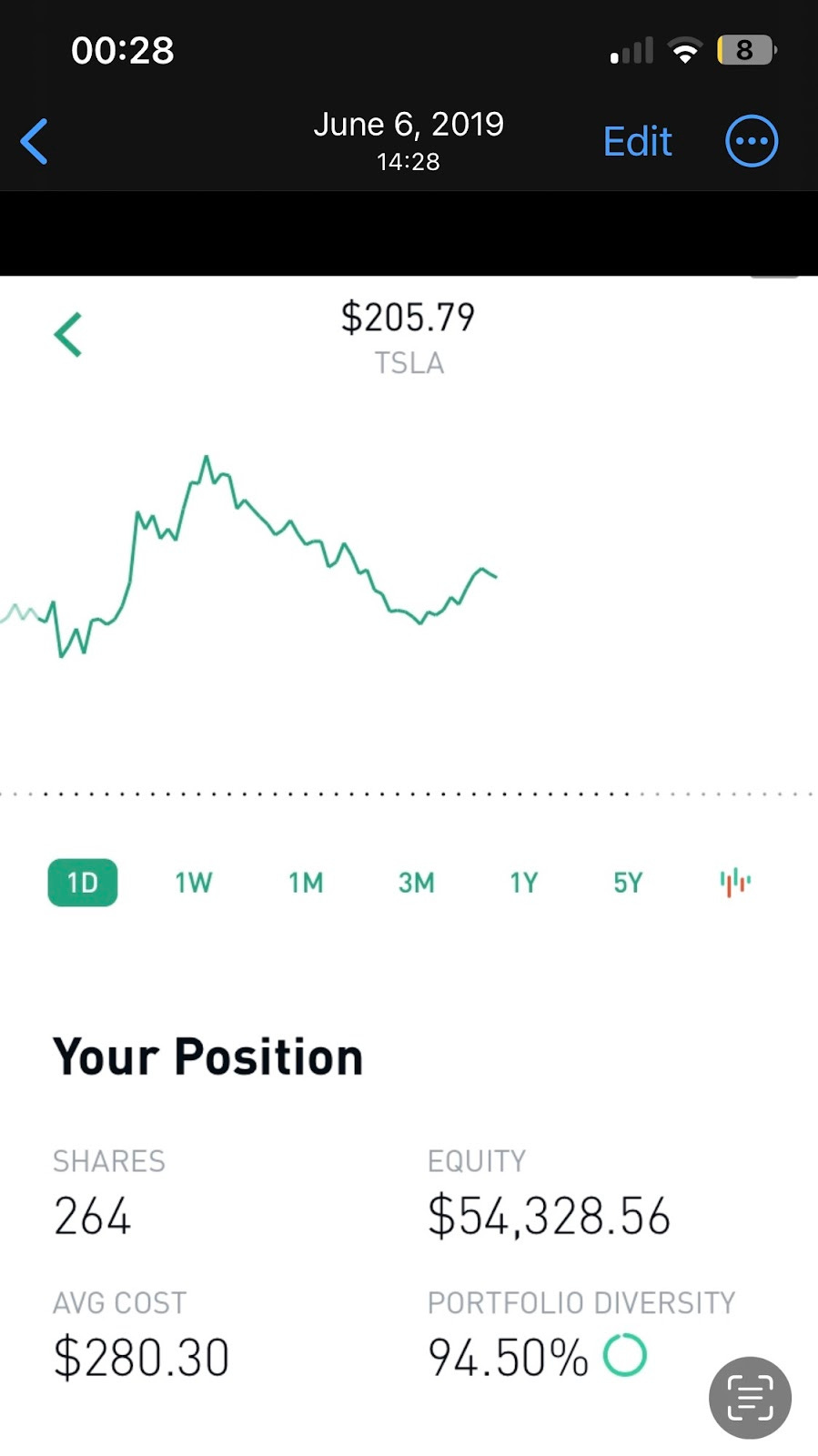

Brokerage Photos

I stumbled across screenshots I took in 2019 of my (LOL) Robinhood account. This was every dollar I could get my hands on. I put my living expenses on a credit card with a 0% promotional rate. This was before the Model 3 program was profitable and before the Model Y was on the roads. Big gains require investing a meaningful amount before the generation of products is scaled and profitable.

After I invested, the stock price dropped. So I bought more.

As you can see, portfolio diversity was 94.5% Tesla. But that doesn’t account for the diversity of businesses within the company that the stock represents. As of writing, Tesla’s market cap is primarily driven by profits from vehicle sales. But in the long term, Tesla’s valuation will be based on a wider basket of businesses. My portfolio for 2024 is more or less the same as 2019.

When I was accumulating shares of Tesla from 2016-2019, there was a big risk of bankruptcy for the fledgling carmaker. That risk is gone. The Model 3/Y program is a hyper-profitable collection of products. But past performance does not guarantee future performance. Interest rates are high and the Fed is unpredictable. But the Tesla team is forged in fire. Strong financials, strong recruiting capability, and Musk-empire cross-pollinations serve as a launch pad for decades of new product creation, including but not limited to, the Dojo supercomputer, a compact car, robotaxi, and Optimus humanoid robots. Every year there will be more advanced robots. What will Tesla invent and scale in the 2030s? HVAC systems? Electric planes?

Just for the hell of it, I’ll do another 5-year prediction. In 2029 Tesla will be valued at $4 trillion.

This essay is not a how-to guide for getting rich. But also, it kind of is. However, none of this is investment advice. If you’d like to talk Tesla with me, message me on X or schedule a curiosity conversation via Calendly.com/ChrisJames3.

If you found this essay useful, entertaining, or both, then consider joining the paid subscribers for $5 a month. I’m writing a book called Inside Elon’s Mind. Paid subscribers will receive a copy.

How to Get Rich (without getting lucky): https://twitter.com/naval/status/1002103360646823936

Thanks for reading

I’m focused on creating truthful, authentic, and useful media. The result is maximum insight through entertainment.

I’m shooting my shot writing books. To support my journey, subscribe here on Substack. Hell, if you're feeling crazy, become a paid subscriber. Paid subs receive free copies of my books.

I’ve done dozens of curiosity conversations with people all around the world which has been amazing. Schedule a call here.

Have a pleasant rest of your day.

Why do you think the market hasn't priced in Tesla's AI/Optimus/EV-adjacent opportunities? I bought in to TSLA back in 2016, and sold in 2021 feeling $1T squarely priced in all those opportunities x uncertainty/risk.

Personally, I'm waiting to see a cohesive strategy of outsourcing with deeper partnerships before buying back in... ala Amazon "sell everything" philosophy or Apple's IP-heavy/manufacturing-light business.

Great essay, Chris! Enjoyed the idea of cross pollination between the companies.

do you think your position would change if any of his other companies really took off (e.g. spacex?)